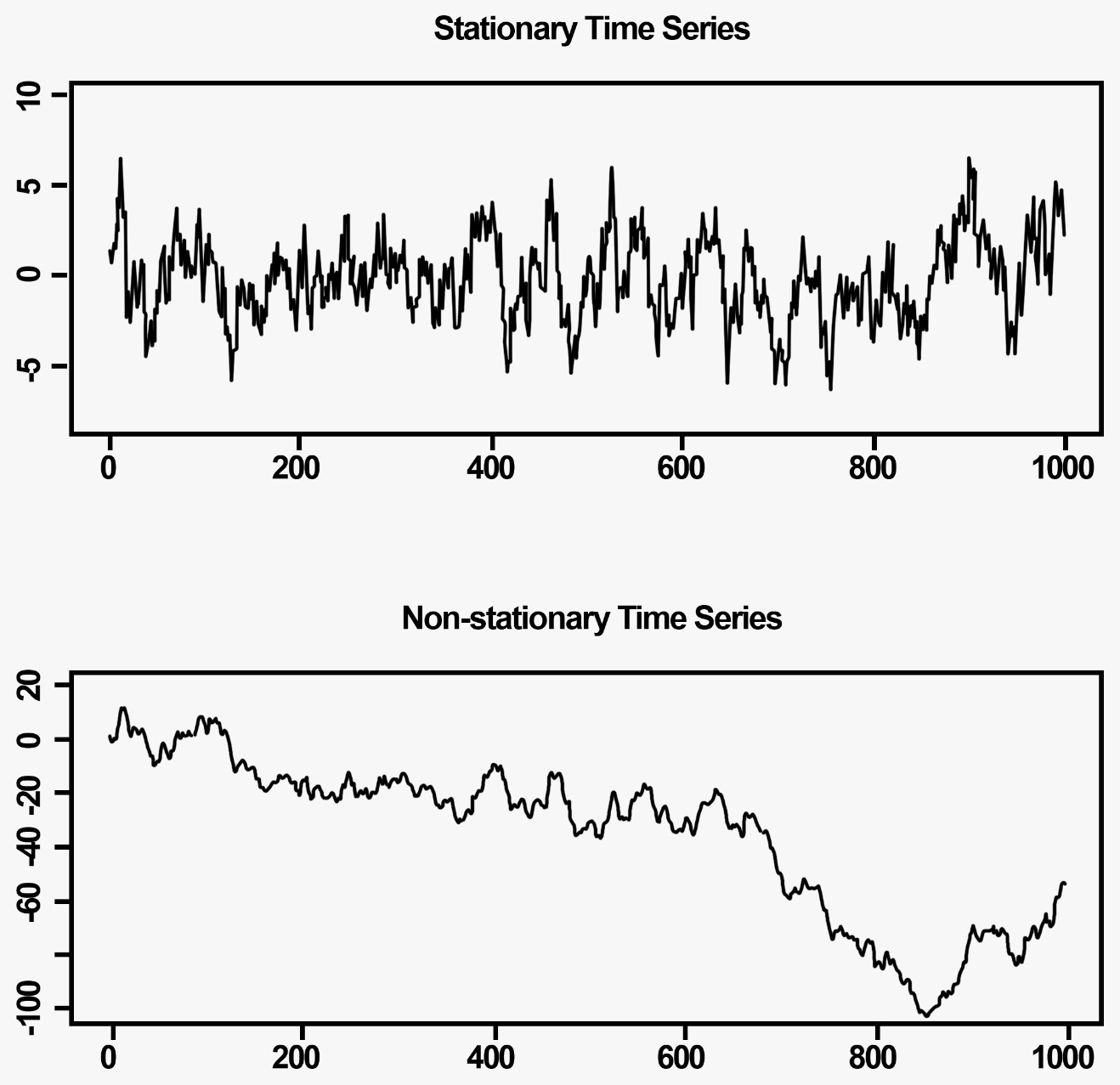

Examples Stationary Time Series . Let \(a\) and \(b\) be uncorrelated random variables with zero mean and. Γ (t + h, t) = cov(x. Web thus, some time series forecasting models, such as autoregressive models, rely on the stationarity of the time series. Web a time series whose statistical properties, such as mean, variance, etc., remain constant over time, are called a. Web introduction to time series analysis. It is stationary if both are. X t+h, xt) = e[(x − μt+h)(x −. Web a time series {xt} has mean function μt = e[xt] and autocovariance function. Web example 1.2.2 (cyclical time series).

from www.oreilly.com

Web thus, some time series forecasting models, such as autoregressive models, rely on the stationarity of the time series. Web introduction to time series analysis. Web a time series whose statistical properties, such as mean, variance, etc., remain constant over time, are called a. Γ (t + h, t) = cov(x. It is stationary if both are. Web a time series {xt} has mean function μt = e[xt] and autocovariance function. Web example 1.2.2 (cyclical time series). X t+h, xt) = e[(x − μt+h)(x −. Let \(a\) and \(b\) be uncorrelated random variables with zero mean and.

Stationarity of a time series models HandsOn Machine Learning for

Examples Stationary Time Series Γ (t + h, t) = cov(x. Γ (t + h, t) = cov(x. Web introduction to time series analysis. X t+h, xt) = e[(x − μt+h)(x −. Let \(a\) and \(b\) be uncorrelated random variables with zero mean and. Web a time series whose statistical properties, such as mean, variance, etc., remain constant over time, are called a. Web a time series {xt} has mean function μt = e[xt] and autocovariance function. Web example 1.2.2 (cyclical time series). Web thus, some time series forecasting models, such as autoregressive models, rely on the stationarity of the time series. It is stationary if both are.

From analystprep.com

Stationary Time Series AnalystPrep FRM Part 1 Study Notes Examples Stationary Time Series Web a time series {xt} has mean function μt = e[xt] and autocovariance function. X t+h, xt) = e[(x − μt+h)(x −. Web thus, some time series forecasting models, such as autoregressive models, rely on the stationarity of the time series. Web a time series whose statistical properties, such as mean, variance, etc., remain constant over time, are called a.. Examples Stationary Time Series.

From analyzingalpha.com

What Is Stationarity? A Visual Guide Analyzing Alpha Examples Stationary Time Series Web thus, some time series forecasting models, such as autoregressive models, rely on the stationarity of the time series. Web a time series whose statistical properties, such as mean, variance, etc., remain constant over time, are called a. Let \(a\) and \(b\) be uncorrelated random variables with zero mean and. Web a time series {xt} has mean function μt =. Examples Stationary Time Series.

From www.oreilly.com

Stationarity of a time series models HandsOn Machine Learning for Examples Stationary Time Series Let \(a\) and \(b\) be uncorrelated random variables with zero mean and. It is stationary if both are. Web introduction to time series analysis. Web thus, some time series forecasting models, such as autoregressive models, rely on the stationarity of the time series. Web a time series {xt} has mean function μt = e[xt] and autocovariance function. Web example 1.2.2. Examples Stationary Time Series.

From otexts.com

9.1 Stationarity and differencing Forecasting Principles and Examples Stationary Time Series X t+h, xt) = e[(x − μt+h)(x −. Web a time series {xt} has mean function μt = e[xt] and autocovariance function. Web example 1.2.2 (cyclical time series). Web thus, some time series forecasting models, such as autoregressive models, rely on the stationarity of the time series. Γ (t + h, t) = cov(x. Web introduction to time series analysis.. Examples Stationary Time Series.

From www.researchgate.net

3 Examples for stationary and nonstationary time series. Download Examples Stationary Time Series It is stationary if both are. Web introduction to time series analysis. Web a time series {xt} has mean function μt = e[xt] and autocovariance function. Let \(a\) and \(b\) be uncorrelated random variables with zero mean and. Web example 1.2.2 (cyclical time series). Web a time series whose statistical properties, such as mean, variance, etc., remain constant over time,. Examples Stationary Time Series.

From devopedia.org

Time Series Analysis Examples Stationary Time Series Γ (t + h, t) = cov(x. Web a time series {xt} has mean function μt = e[xt] and autocovariance function. X t+h, xt) = e[(x − μt+h)(x −. It is stationary if both are. Let \(a\) and \(b\) be uncorrelated random variables with zero mean and. Web a time series whose statistical properties, such as mean, variance, etc., remain. Examples Stationary Time Series.

From www.slideserve.com

PPT Stationarity, Non Stationarity, Unit Roots and Spurious Examples Stationary Time Series Web a time series whose statistical properties, such as mean, variance, etc., remain constant over time, are called a. Web thus, some time series forecasting models, such as autoregressive models, rely on the stationarity of the time series. It is stationary if both are. Web example 1.2.2 (cyclical time series). Web a time series {xt} has mean function μt =. Examples Stationary Time Series.

From datascience.stackexchange.com

machine learning How is cyclic time series data stationary Data Examples Stationary Time Series Web a time series {xt} has mean function μt = e[xt] and autocovariance function. It is stationary if both are. Web introduction to time series analysis. Γ (t + h, t) = cov(x. X t+h, xt) = e[(x − μt+h)(x −. Web a time series whose statistical properties, such as mean, variance, etc., remain constant over time, are called a.. Examples Stationary Time Series.

From www.analytixlabs.co.in

Time Series Analysis & Forecasting Guide AnalytixLabs Examples Stationary Time Series Web thus, some time series forecasting models, such as autoregressive models, rely on the stationarity of the time series. It is stationary if both are. Γ (t + h, t) = cov(x. Web introduction to time series analysis. X t+h, xt) = e[(x − μt+h)(x −. Let \(a\) and \(b\) be uncorrelated random variables with zero mean and. Web a. Examples Stationary Time Series.

From www.slideserve.com

PPT Time Series Econometrics PowerPoint Presentation, free download Examples Stationary Time Series Let \(a\) and \(b\) be uncorrelated random variables with zero mean and. It is stationary if both are. X t+h, xt) = e[(x − μt+h)(x −. Web example 1.2.2 (cyclical time series). Web introduction to time series analysis. Γ (t + h, t) = cov(x. Web a time series {xt} has mean function μt = e[xt] and autocovariance function. Web. Examples Stationary Time Series.

From www.researchgate.net

3 Examples for stationary and nonstationary time series. Download Examples Stationary Time Series Web a time series {xt} has mean function μt = e[xt] and autocovariance function. Γ (t + h, t) = cov(x. Web thus, some time series forecasting models, such as autoregressive models, rely on the stationarity of the time series. Let \(a\) and \(b\) be uncorrelated random variables with zero mean and. Web introduction to time series analysis. Web a. Examples Stationary Time Series.

From www.youtube.com

Checking Stationarity of a Time Series YouTube Examples Stationary Time Series Web a time series whose statistical properties, such as mean, variance, etc., remain constant over time, are called a. Let \(a\) and \(b\) be uncorrelated random variables with zero mean and. It is stationary if both are. X t+h, xt) = e[(x − μt+h)(x −. Web thus, some time series forecasting models, such as autoregressive models, rely on the stationarity. Examples Stationary Time Series.

From stats.stackexchange.com

time series Stationarity Tests in R, checking mean, variance and Examples Stationary Time Series Let \(a\) and \(b\) be uncorrelated random variables with zero mean and. It is stationary if both are. Web introduction to time series analysis. Web a time series whose statistical properties, such as mean, variance, etc., remain constant over time, are called a. Web thus, some time series forecasting models, such as autoregressive models, rely on the stationarity of the. Examples Stationary Time Series.

From www.gaussianwaves.com

AutoCorrelation (Correlogram) and persistence Time series analysis Examples Stationary Time Series Web a time series whose statistical properties, such as mean, variance, etc., remain constant over time, are called a. Let \(a\) and \(b\) be uncorrelated random variables with zero mean and. Web thus, some time series forecasting models, such as autoregressive models, rely on the stationarity of the time series. Web introduction to time series analysis. Γ (t + h,. Examples Stationary Time Series.

From www.slideserve.com

PPT Time Series Analysis PowerPoint Presentation, free download ID Examples Stationary Time Series Γ (t + h, t) = cov(x. Web a time series whose statistical properties, such as mean, variance, etc., remain constant over time, are called a. Web introduction to time series analysis. Web a time series {xt} has mean function μt = e[xt] and autocovariance function. It is stationary if both are. Web thus, some time series forecasting models, such. Examples Stationary Time Series.

From www.researchgate.net

3 Examples for stationary and nonstationary time series. Download Examples Stationary Time Series It is stationary if both are. Web a time series {xt} has mean function μt = e[xt] and autocovariance function. Web example 1.2.2 (cyclical time series). Web thus, some time series forecasting models, such as autoregressive models, rely on the stationarity of the time series. X t+h, xt) = e[(x − μt+h)(x −. Web introduction to time series analysis. Web. Examples Stationary Time Series.

From towardsdatascience.com

Time Series Analysis and Climate Change Towards Data Science Examples Stationary Time Series Web thus, some time series forecasting models, such as autoregressive models, rely on the stationarity of the time series. X t+h, xt) = e[(x − μt+h)(x −. Web a time series whose statistical properties, such as mean, variance, etc., remain constant over time, are called a. Web introduction to time series analysis. Web example 1.2.2 (cyclical time series). Web a. Examples Stationary Time Series.

From blog.quantinsti.com

Stationarity in Time Series Analysis Explained using Python Examples Stationary Time Series X t+h, xt) = e[(x − μt+h)(x −. Web thus, some time series forecasting models, such as autoregressive models, rely on the stationarity of the time series. Web example 1.2.2 (cyclical time series). It is stationary if both are. Web a time series {xt} has mean function μt = e[xt] and autocovariance function. Web a time series whose statistical properties,. Examples Stationary Time Series.